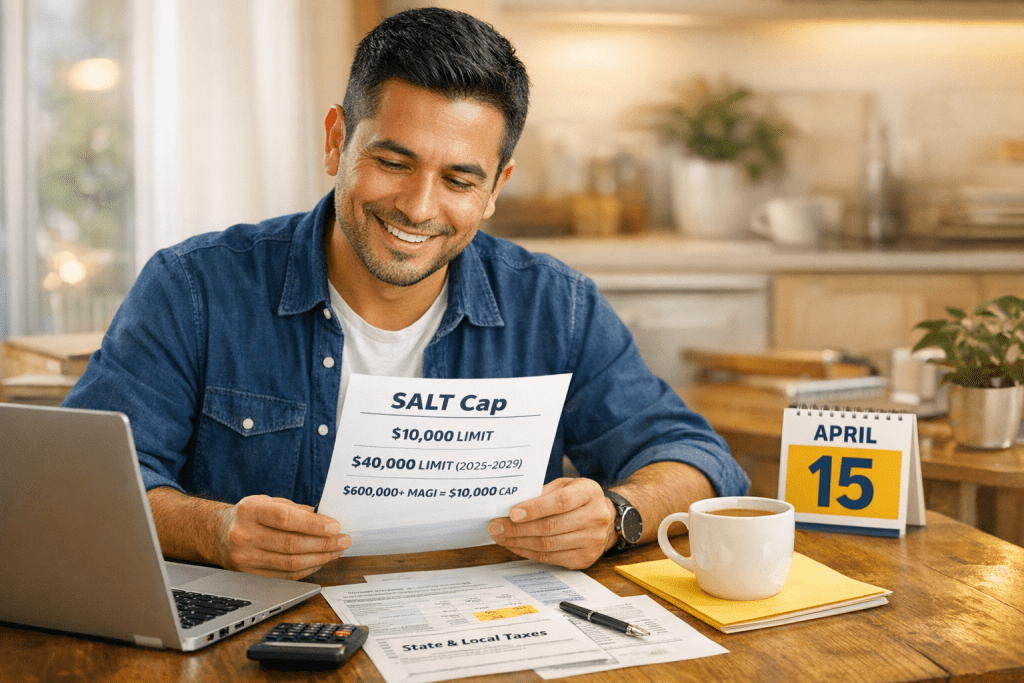

The SALT cap explained simply: federal law sets a ceiling on your deduction for state and local taxes (state income tax plus property tax combined). From 2018 through 2024, that ceiling was $10,000. For 2025 through 2029, the One Big Beautiful Bill Act raised it to $40,000 per return ($20,000 if married filing separately), but the cap phases down for higher earners and reverts to $10,000 for filers with modified adjusted gross income (MAGI) above $600,000. MAGI is your adjusted gross income plus certain excluded income items like foreign earnings. Understanding where you fall determines how much this rule actually costs you.

TL;DR

- SALT stands for State And Local Taxes, covering state income tax, property tax, and sometimes local sales tax.

- The SALT deduction cap is $40,000 per return for 2025-2029 ($20,000 if married filing separately), up from $10,000 under the original TCJA rule. It phases down for MAGI above $500,000 and drops back to $10,000 at $600,000+.

- The cap still hits hardest in CA, NY, NJ, CT, and MA, where combined taxes can exceed even the higher limit for upper-income households.

- The cap only matters if you itemize; about 90% of filers benefit more from the standard deduction anyway.

- A deductible Traditional IRA contribution can lower your AGI before any deduction caps even come into play, and may help you stay below the MAGI phaseout threshold.

Why Your Refund Felt Wrong This Year

You held up your end. State income taxes, paid. Property taxes, paid. And then the refund arrived smaller than expected, or worse, a balance showed up that you hadn’t budgeted for. That disconnect between what you paid and what you got back isn’t random. It has a specific cause, and understanding it now gives you months to prepare before the next filing deadline.

If you live in a high-tax state, the SALT cap explained in this guide fills in the gap most people are missing. The state and local tax deduction is now capped at $40,000 for most filers under the One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025. That sounds like a big improvement over the old $10,000 cap, and for many households it is. But for high-income filers in states like California, New York, New Jersey, or Massachusetts, the cap still phases down and can revert to $10,000 once MAGI exceeds $600,000. Below, we break down exactly how the cap works, who absorbs the hit, and the concrete moves you can make to plan around it.

What this means for your money

The SALT cap doesn’t touch what you owe your state; it limits how much of that payment offsets your federal taxes. When the deduction gets cut off, your taxable income stays elevated, which means a thinner refund or a steeper bill in April. The upside: once you see the cap clearly, you can start building a plan that works within these rules rather than getting blindsided by them year after year.

What Is the SALT Deduction?

SALT stands for State And Local Taxes. On your federal return, this deduction covers three types of payments: state income tax (or state sales tax if you elect that option), local income tax, and real estate property tax. Before 2018, there was no ceiling; if you itemized, you could deduct every dollar of those taxes.

The Tax Cuts and Jobs Act (TCJA), a federal tax reform law signed in 2017, changed that. Starting with the 2018 tax year, the IRS began enforcing a $10,000 cap on the total SALT deduction ($5,000 if married filing separately). That original cap stayed in place through the 2024 tax year. Then the OBBBA, signed on July 4, 2025, raised the ceiling to $40,000 ($20,000 MFS) for 2025 through 2029. The cap may be adjusted over time, depending on future guidance and inflation adjustments.. Starting in 2030, the cap is scheduled to drop back to $10,000 unless Congress acts again.

How Does the SALT Cap Work, and Where Does the Deduction Go?

The arithmetic is straightforward. Add up your state income tax withheld, your property tax bill, and any local taxes. If the total falls under the cap for your income level, you deduct it all (assuming you itemize). If it exceeds your cap, every dollar above that line is simply gone; you cannot apply it anywhere else on your federal return.

For most filers with MAGI below $500,000, the cap is $40,000 in 2025. But the cap shrinks by 30 cents for every dollar your MAGI exceeds $500,000. Once MAGI hits $600,000 or more, the cap drops to $10,000, the same limit that existed before the OBBBA. Some tax experts call this income range the “SALT torpedo” because the phaseout creates an artificially high effective tax rate. That lost excess is real money off the table. Depending on your federal tax bracket, each forfeited dollar translates directly into additional federal tax owed.

Consider what that looks like across three simplified, illustrative scenarios for a household filing jointly in 2025:

- $90,000 income (high-tax state): State income tax ~$5,000. Property tax ~$7,500. Total SALT: $12,500. Under the $40,000 cap, so the full amount is deductible if itemizing. But the standard deduction is $31,500 for married couples filing jointly, so total itemized deductions need to exceed that threshold to make itemizing worthwhile.

- $200,000 income (high-tax state): State income tax ~$12,000. Property tax ~$12,000. Total SALT: $24,000. Under the $40,000 cap, fully deductible. Combined with mortgage interest and other deductions, itemizing likely makes sense here.

- $550,000 income (high-tax state): State income tax ~$40,000. Property tax ~$15,000. Total SALT: $55,000. MAGI is $50,000 over the $500,000 threshold, so the $40,000 cap is reduced by $15,000 (30% × $50,000), leaving a cap of $25,000. Lost deduction: $30,000. At the 35% bracket, that adds up to roughly $10,500 in additional federal taxes.

The Misconception Nobody Warns You About

Many people assume the raised SALT cap fixed everything. For middle-income households in high-tax states, it largely did. But for earners near or above $500,000, the phaseout creates a new layer of complexity. Your cap shrinks as your income grows, and at $600,000 you’re right back at $10,000, the same ceiling that existed from 2018 through 2024.

Think of it like a coupon with a variable discount based on your income. The higher you earn, the smaller the coupon gets. Coming to terms with your specific cap, based on your MAGI, is the necessary first step toward planning around it effectively.

There’s a second layer that catches many people off guard: the SALT deduction only helps if you itemize at all. Since the TCJA nearly doubled the standard deduction, far fewer households cross that threshold. For 2025, the standard deduction sits at $15,750 for single filers and $31,500 for married couples filing jointly (as adjusted by the OBBBA). If your total itemized deductions, including mortgage interest, charitable contributions, and your capped SALT amount, don’t clear those numbers, the standard deduction delivers a bigger tax break. According to IRS filing data, roughly 90% of filers now take the standard deduction. For most of them, the SALT cap never shows up on their return at all.

What Can You Do Instead?

You can’t negotiate this cap away. But you can redirect your attention to the levers that still move.

Review your withholding. If your refund shrank or you owed an unexpected balance, your W-4 may be overdue for an update. Adjusting withholding doesn’t alter your total tax bill; it eliminates the surprise and lets you manage cash flow steadily throughout the year instead of scrambling in April.

Consider eligible retirement contributions. A Traditional IRA contribution, when deductible, reduces your adjusted gross income (AGI), which is your total income minus certain deductions, before the standard or itemized deduction even enters the equation. For 2025, the IRS allows up to $7,000 per person ($8,000 if you’re 50 or older). Whether you qualify for the full deduction depends on your income and whether you or your spouse are covered by a workplace retirement plan; eligibility varies. But when it applies, it’s one of the few tools that cuts your taxable income at the source, before caps and deductions factor in. Lower AGI also helps you stay below the $500,000 MAGI threshold where the SALT cap starts shrinking.

Plan before April, not during it. Most tax surprises grow out of stale assumptions, like assuming the rules stayed the same. Building a habit of reviewing your tax picture mid-year remains the most dependable way to avoid the shock when filing season arrives.

Frequently Asked Questions

What is the SALT cap and how is it explained for regular filers?

The SALT cap limits the state and local tax deduction on your federal return. For 2025 through 2029, the cap is $40,000 per return ($20,000 if married filing separately), raised from $10,000 by the legislation commonly referred to as the “Big Beautiful Bill,” signed on July 4, 2025. The cap may change over time based on future adjustments and guidance. However, filers with modified adjusted gross income above $500,000 will see the cap phase down gradually as income increases, eventually reaching $10,000 at higher income levels. Starting in 2030, the cap is scheduled to revert to $10,000 for all filers.

Does the SALT cap apply if I take the standard deduction?

No. SALT only matters when you itemize. If your total itemized deductions, including mortgage interest, charitable contributions, and the capped SALT amount, don’t exceed the standard deduction ($15,750 single or $31,500 married filing jointly for 2025), the cap is irrelevant. You’d take the standard deduction instead. About 90% of filers currently choose the standard deduction, according to IRS statistics of income data.

Which states are hit hardest by the SALT deduction limit?

Households in California, New York, New Jersey, Connecticut, and Massachusetts feel the cap most acutely. Even with the higher $40,000 limit, upper-income filers in these states often hit the MAGI phaseout, reducing their effective cap well below $40,000. Some tax professionals refer to the $500,000-$600,000 income range as the “SALT torpedo” because the phaseout creates an artificially high effective tax rate in that band. For earners above $600,000, the cap is $10,000 regardless of state, making this a continued pain point for high-income households in high-tax states.

Can a Traditional IRA help if the SALT cap reduces my deduction?

A deductible Traditional IRA contribution lowers your AGI before itemized deductions are calculated. If eligible (depending on income and workplace plan coverage), it can reduce taxable income by up to $7,000 in 2025 ($8,000 if you’re 50+), regardless of whether you itemize. It can also help keep your MAGI below the $500,000 threshold where the SALT cap starts shrinking. You can learn more about why your tax bill may have changed this year for additional context.

When you’re ready to look at what’s still within your control, Finhabits offers tools to help you understand IRA contribution limits and build a retirement plan that works alongside your tax reality, not against it.

Turning Frustration Into a Plan

The SALT cap explained in one sentence: the federal government limits how much of your state and local taxes you can deduct, and that limit depends on your income. For most filers, the 2025 cap is $40,000, but it shrinks for higher earners and drops back to $10,000 in 2030. You can’t rewrite the rule, but you can stop letting it catch you flat-footed. Know your deduction limits. Evaluate whether itemizing genuinely makes sense for your situation. Explore eligible ways to lower your AGI before deductions even apply.

The households who feel most in command of their taxes aren’t necessarily the ones collecting the biggest refunds. They’re the ones who planned ahead, absorbed the rules as they actually stand, and built steady habits that compound over time, because that kind of consistency is worth more than any single deduction.

Sources

- Internal Revenue Service (IRS) – Topic no. 503, Deductible taxes

- Internal Revenue Service (IRS) – SOI tax stats: What’s new

All sources accessed and verified on 2026-03-26. External links open in new window.

Disclaimer:

This material is provided for informational purposes only and is not intended to offer investment, legal, or tax advice. All images and figures are for illustrative purposes. Investment advisory services are offered through Finhabits Advisors LLC, a registered investment advisor with the SEC. Registration does not imply a certain level of skill or training. Past performance is not indicative of future returns. All investments involve risk, including the possible loss of principal. Securities are offered through Apex Clearing Corporation, a Member of FINRA and SIPC. Securities held at Apex are protected up to $500,000, which includes a $250,000 cash limit. See SIPC.org for more details.

Projections are for educational and illustrative purposes only. They are based on the assumptions stated and will change if those assumptions change. They do not predict or reflect the actual performance of any Finhabits portfolio, and they do not account for economic, market, or individual financial factors that can impact real investment outcomes.

For tax-related questions, consult a qualified tax professional and refer to the official information available on the IRS website (irs.gov).

© Finhabits, Inc. All rights reserved.